A large class of economic models involves solving for functional equations of the form:

A well known example is the stochastic optimal growth model. An agent owns a consumption good $y$ at time $t$, which can be consumed or invested. Next period’s output depends on how much is invested at time $t$ and on a shock $z$ realized at the end of the current period. One can think of a farmer deciding the quantity of seeds to be planted during the spring, taking into account weather forecast for the growing season.

A common technique for solving this class of problem is value function iteration. While value function iteration is quite intuitive, it is not the only one available. In this post, I describe the collocation method, which transforms the problem of finding a function into a problem of finding a vector that satisfies a given set of conditions. The gain from this change of perspective is that any root-finding algorithm can then be used. In particular, one may use the Newton method, which converges at a quadratic rate in the neighborhood of the solution if the function is smooth enough.

Value function iteration

Value function iteration takes advantage of the fact that the Bellman operator $T$ is a contraction mapping on the set of continuous bounded functions on $\mathbb R_+$ under the supremum distance

An immediate consequence if that the sequence $w,Tw,T^2w$,… converges uniformly to $w$ (starting with any bounded and continuous function $w$). The following code in

An immediate consequence if that the sequence $w,Tw,T^2w$,… converges uniformly to $w$ (starting with any bounded and continuous function $w$). The following code in Julia v0.6.4 illustrates the convergence of the series ${T^nw}$.

#=

Julien Pascal

Code heavily based on:

----------------------

https://lectures.quantecon.org/jl/optgrowth.html

by Spencer Lyon, John Stachurski

I have only made minor modifications:

#------------------------------------

* I added a type optGrowth

* I use the package Interpolations

* I calculate the expectation w.r.t the aggregate

shock using a Gauss-Legendre quadrature scheme

instead of Monte-Carlo

=#

using QuantEcon

using Optim

using CompEcon

using PyPlot

using Interpolations

using FileIO

type optGrowth

w::Array{Float64,1}

β::AbstractFloat

grid::Array{Float64,1}

u::Function

f::Function

shocks::Array{Float64,1}

Tw::Array{Float64,1}

σ::Array{Float64,1}

el_k::Array{Float64,1}

wl_k::Array{Float64,1}

compute_policy::Bool

w_func::Function

end

function optGrowth(;w = Array{Float64,1}[],

α = 0.4,

β = 0.96,

μ = 0,

s = 0.1,

grid_max = 4, # Largest grid point

grid_size = 200, # Number of grid points

shock_size = 250, # Number of shock draws in Monte Carlo integral

Tw = Array{Float64,1}[],

σ = Array{Float64,1}[],

el_k = Array{Float64,1}[],

wl_k = Array{Float64,1}[],

compute_policy = true

)

grid_y = collect(linspace(1e-5, grid_max, grid_size))

shocks = exp.(μ + s * randn(shock_size))

# Utility

u(c) = log(c)

# Production

f(k) = k^α

w = 5 * log.(grid_y)

Tw = 5 * log.(grid_y)

σ = 5 * log.(grid_y)

el_k, wl_k = qnwlogn(10, μ, s^2) #10 weights and nodes for LOG(e_t) distributed N(μ,s^2)

w_func = x -> x

optGrowth(

w,

β,

grid_y,

u,

f,

shocks,

Tw,

σ,

el_k,

wl_k,

compute_policy,

w_func

)

end

"""

The approximate Bellman operator, which computes and returns the

updated value function Tw on the grid points.

#### Arguments

`model` : a model of type optGrowth

`Modifies model.σ, model.w and model.Tw

"""

function bellman_operator!(model::optGrowth)

# === Apply linear interpolation to w === #

knots = (model.grid,)

itp = interpolate(knots, model.w, Gridded(Linear()))

#w_func(x) = itp[x]

model.w_func = x -> itp[x]

if model.compute_policy

model.σ = similar(model.w)

end

# == set Tw[i] = max_c { u(c) + β E w(f(y - c) z)} == #

for (i, y) in enumerate(model.grid)

#Monte Carlo

#-----------

#objective(c) = - model.u(c) - model.β * mean(w_func(model.f(y - c) .* model.shocks))

#Gauss-Legendre

#--------------

function objective(c)

expectation = 0.0

for k = 1:length(model.wl_k)

expectation += model.wl_k[k]*(model.w_func(model.f(y - c) * model.el_k[k]))

end

- model.u(c) - model.β * expectation

end

res = optimize(objective, 1e-10, y)

if model.compute_policy

model.σ[i] = Optim.minimizer(res)

end

model.Tw[i] = - Optim.minimum(res)

model.w[i] = - Optim.minimum(res)

end

end

model = optGrowth()

function solve_optgrowth!(model::optGrowth;

tol::AbstractFloat=1e-6,

max_iter::Integer=500)

w_old = copy(model.w) # Set initial condition

error = tol + 1

i = 0

# Iterate to find solution

while i < max_iter

#update model.w

bellman_operator!(model)

error = maximum(abs, model.w - w_old)

if error < tol

break

end

w_old = copy(model.w)

i += 1

end

end

#-----------------------------------

# Solve by value function iteration

#-----------------------------------

@time solve_optgrowth!(model)

# 3.230501 seconds (118.18 M allocations: 1.776 GiB, 3.51% gc time)

#-------------------------------

# Compare with the true solution

#-------------------------------

α = 0.4

β = 0.96

μ = 0

s = 0.1

c1 = log(1 - α * β) / (1 - β)

c2 = (μ + α * log(α * β)) / (1 - α)

c3 = 1 / (1 - β)

c4 = 1 / (1 - α * β)

# True optimal policy

c_star(y) = (1 - α * β) * y

# True value function

v_star(y) = c1 + c2 * (c3 - c4) + c4 * log.(y)

fig, ax = subplots(figsize=(9, 5))

ax[:set_ylim](-35, -24)

ax[:plot](model.grid, model.w_func.(model.grid), lw=2, alpha=0.6, label="Approximated (VFI)", linestyle="--")

ax[:plot](model.grid, v_star.(model.grid), lw=2, alpha=0.6, label="Exact value")

ax[:legend](loc="lower right")

savefig("value_function_iteration.png")

fig, ax = subplots(figsize=(9, 5))

ax[:set_xlim](0.1, 4.0)

ax[:set_ylim](0.00, 0.008)

ax[:plot](model.grid, abs.(model.w_func.(model.grid) -v_star.(model.grid)), lw=2, alpha=0.6, label="error")

ax[:legend](loc="lower right")

savefig("error_value_function_iteration.png")

Output

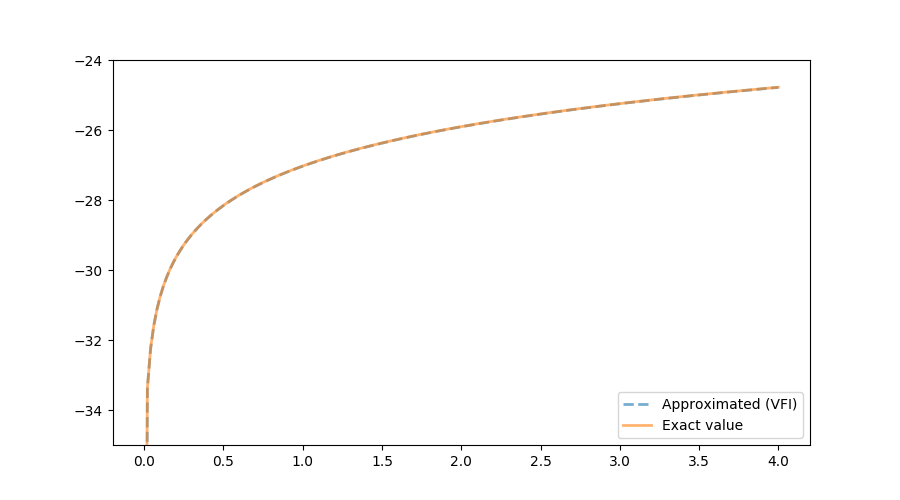

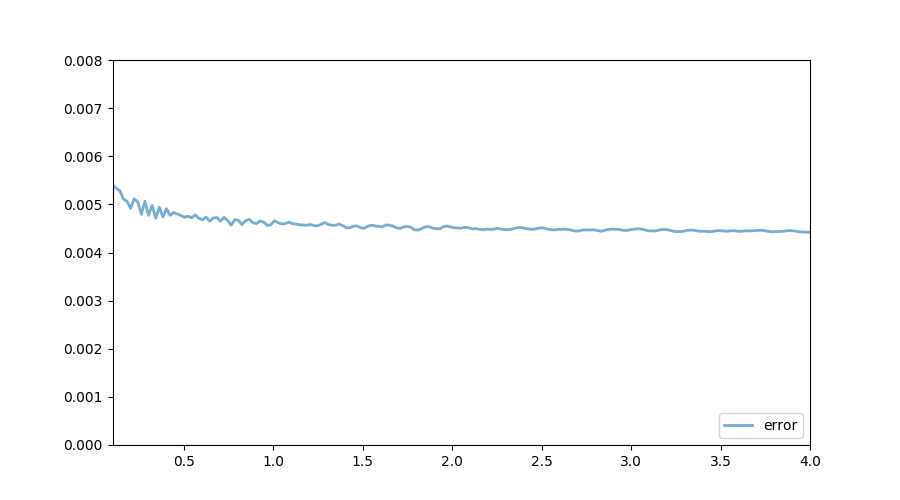

The following figure shows the exact function, which we know in this very specific case, and the one calculated using VFI. Both quantities are almost indistinguishable. As the illustrated in the next figure, the (absolute value) of the distance between the true and the approximated values is bounded above by $0.006$. The accuracy of the current approximation could be improved by iterating the process further.

The collocation method

The collocation method takes a different route. Let us remember that we are looking for a function $w$. Instead of solving for the values of $w$ on a grid and then interpolating, why not looking for a function directly? To do so, let us assume that $w$ can reasonably be approximated by a function $\hat{w}$:

with $ \phi_1(x) $ , $ \phi_2(x) $,…, $ \phi_n(x) $ a set of linearly independent basis functions and $c_1$, $c_2$, …, $c_n$ $n$ coefficient to be found. Replacing $w(x)$ with $\hat{w(x)}$ into the functional equation and reorganizing gives:

This equation has to hold (almost) exactly at $n$ points (also called nodes): $y_1$, $y_2$, …, $y_n$:

The equation above defines a system of $n$ equation with as many unknown, which can be compactly written as: $$ f(\boldsymbol{c}) = \boldsymbol{0} $$

Newton or quasi-Newton can be used to solve for the root of $f$. In the code that follows, I use Broyden’s method. Let us illustrate this technique using a Chebychev polynomial basis and Chebychev nodes. In doing so, we avoid Runge’s phenomenon associated with a uniform grid.

Implementation using CompEcon

#---------------------------------------------

# Julien Pascal

# Solve the stochastic optimal growth problem

# using the collocation method

#---------------------------------------------

using QuantEcon

using Optim

using CompEcon

using PyPlot

using Interpolations

type optGrowthCollocation

w::Array{Float64,1}

β::AbstractFloat

grid::Array{Float64,1}

u::Function

f::Function

shocks::Array{Float64,1}

Tw::Array{Float64,1}

σ::Array{Float64,1}

el_k::Array{Float64,1}

wl_k::Array{Float64,1}

compute_policy::Bool

order_approximation::Int64 #number of element in the functional basis along each dimension

functional_basis_type::String #type of functional basis

fspace::Dict{Symbol,Any} #functional basis

fnodes::Array{Float64,1} #collocation nodes

residual::Array{Float64,1} #vector of residual. Should be close to zero

a::Array{Float64,1} #polynomial coefficients

w_func::Function

end

#####################################

# Function that finds a solution

# to f(x) = 0

# using Broyden's "good" method

# and a simple backstepping procedure as described

# in Miranda and Fackler (2009)

#

# input :

# --------

# * x0: initial guess for the root

# * f: function in f(x) = 0

# * maxit: maximum number of iterations

# * tol: tolerance level for the zero

# * fjavinc: initial inverse of the jacobian. If not provided, then inverse of the

# Jacobian is calculated by finite differences

# * maxsteps: maximum number of backsteps

# * recaculateJacobian: number of iterations in-between two calculations of the Jacobian

#

# output :

# --------

# * x: one zero of f

# * it: number of iterations necessary to reached the solution

# * fjacinv: pseudo jacobian at the last iteration

# * fnorm: norm f(x) at the last iteration

#

#######################################

function find_broyden(x0::Vector, f::Function, maxit::Int64, tol::Float64, fjacinv = eye(length(x0));

maxsteps = 5, recaculateJacobian = 1)

println("a0 = $(x0)")

fnorm = tol*2

it2 = 0 #to re-initialize the jacobian

################################

#initialize guess for the matrix

################################

fjacinv_function = x-> Calculus.finite_difference_jacobian(f, x)

#fjacinv_function = x -> ForwardDiff.gradient(f, x)

# If the user do not provide an initial guess for the jacobian

# One is calculated using finite differences.

if fjacinv == eye(length(x0))

################################################

# finite differences to approximate the Jacobian

# at the initial value

# this is slow. Seems to improve performances

# when x0 is of high dimension.

println("Calculating the Jacobian by finite differences")

#@time fjacinv = Calculus.finite_difference_jacobian(f, x0)

@time fjacinv = fjacinv_function(x0)

println("Inverting the Jacobian")

try

fjacinv = inv(fjacinv)

catch

try

println("Jacobian non-invertible\n calculating pseudo-inverse")

fjacinv = pinv(A)

catch

println("Failing Calculating the pseudo-inverse. Initializing with In")

fjacinv = eye(length(x0))

end

end

println("Done")

else

println("Using User's input as a guess for the Jacobian.")

end

fval = f(x0)

for it=1:maxit

it2 +=1

#every 30 iterations, reinitilize the jacobian

if mod(it2, recaculateJacobian) == 0

println("Re-calculating the Jacobian")

fjacinv = fjacinv_function(x0)

try

fjacinv = inv(fjacinv)

catch

try

println("Jacobian non-invertible\n calculating pseudo-inverse")

fjacinv = pinv(A)

catch

println("Failing Calculating the pseudo-inverse. Initializing with In")

fjacinv = eye(length(x0))

end

end

end

println("it = $(it)")

fnorm = norm(fval)

if fnorm < tol

println("fnorm = $(fnorm)")

return x0, it, fjacinv, fnorm

end

d = -(fjacinv*fval)

fnormold = Inf

########################

# Backstepping procedure

########################

for backstep = 1:maxsteps

if backstep > 1

println("backstep = $(backstep-1)")

end

fvalnew = f(x0 + d)

fnormnew = norm(fvalnew)

if fnormnew < fnorm

break

end

if fnormold < fnormnew

d=2*d

break

end

fnormold = fnormnew

d = d/2

end

####################

####################

x0 = x0 + d

fold = fval

fval = f(x0)

u = fjacinv*(fval - fold)

#Update the pseudo Jacobian:

fjacinv = fjacinv + ((d-u)*(transpose(d)*fjacinv))/(dot(d,u))

println("a$(it) = $(x0)")

println("fnorm = $(fnorm)")

if isnan.(x0) == trues(length(x0))

println("Error. a$(it) = NaN for each component")

x0 = zeros(length(x0))

return x0, it, fjacinv, fnorm

end

end

println("In function find_broyden\n")

println("Maximum number of iterations reached.\n")

println("No convergence.")

println("Returning fnorm = NaN as a solution")

fnorm = NaN

return x0, maxit, fjacinv, fnorm

end

function optGrowthCollocation(;w = Array{Float64,1}[],

α = 0.4,

β = 0.96,

μ = 0,

s = 0.1,

grid_max = 4, # Largest grid point

grid_size = 200, # Number of grid points

shock_size = 250, # Number of shock draws in Monte Carlo integral

Tw = Array{Float64,1}[],

σ = Array{Float64,1}[],

el_k = Array{Float64,1}[],

wl_k = Array{Float64,1}[],

compute_policy = true,

order_approximation = 40,

functional_basis_type = "chebychev",

)

grid_y = collect(linspace(1e-5, grid_max, grid_size))

shocks = exp.(μ + s * randn(shock_size))

# Utility

u(c) = log.(c)

# Production

f(k) = k^α

el_k, wl_k = qnwlogn(10, μ, s^2) #10 weights and nodes for LOG(e_t) distributed N(μ,s^2)

lower_bound_support = minimum(grid_y)

upper_bound_support = maximum(grid_y)

n_functional_basis = [order_approximation]

if functional_basis_type == "chebychev"

fspace = fundefn(:cheb, n_functional_basis, lower_bound_support, upper_bound_support)

elseif functional_basis_type == "splines"

fspace = fundefn(:spli, n_functional_basis, lower_bound_support, upper_bound_support, 1)

elseif functional_basis_type == "linear"

fspace = fundefn(:lin, n_functional_basis, lower_bound_support, upper_bound_support)

else

error("functional_basis_type has to be either chebychev, splines or linear.")

end

fnodes = funnode(fspace)[1]

residual = zeros(size(fnodes)[1])

a = ones(size(fnodes)[1])

w = ones(size(fnodes)[1])

Tw = ones(size(fnodes)[1])

σ = ones(size(fnodes)[1])

w_func = x-> x

optGrowthCollocation(

w,

β,

grid_y,

u,

f,

shocks,

Tw,

σ,

el_k,

wl_k,

compute_policy,

order_approximation,

functional_basis_type,

fspace,

fnodes,

residual,

a,

w_func

)

end

function residual!(model::optGrowthCollocation)

model.w_func = y -> funeval(model.a, model.fspace, [y])[1][1]

function objective(c, y)

expectation = 0.0

for k = 1:length(model.wl_k)

expectation += model.wl_k[k]*(model.w_func(model.f(y - c) * model.el_k[k]))

end

- model.u(c) - model.β * expectation

end

# Loop over nodes

for i in 1:size(model.fnodes)[1]

y = model.fnodes[i,1]

res = optimize(c -> objective(c, y), 1e-10, y)

if model.compute_policy

model.σ[i] = Optim.minimizer(res)

end

model.Tw[i] = - Optim.minimum(res)

model.w[i] = model.w_func(y)

model.residual[i] = - model.w[i] + model.Tw[i]

end

end

model = optGrowthCollocation(functional_basis_type = "chebychev")

residual!(model)

function solve_optgrowth!(model::optGrowthCollocation;

tol=1e-6,

max_iter=500)

# Initialize guess for coefficients

# by giving the "right shape"

# ---------------------------------

function objective_initialize!(x, model)

#update polynomial coeffficients

model.a = copy(x)

model.w_func = y -> funeval(model.a, model.fspace, [y])[1][1]

return abs.(model.w_func.(model.fnodes[:,1]) - 5.0 * log.(model.fnodes[:,1]))

end

minx, iterations, Jac0, fnorm = find_broyden(model.a, x -> objective_initialize!(x, model), max_iter, tol)

# Solving the model by collocation

# using the initial guess calculated above

#-----------------------------------------

function objective_residual!(x, model)

#update polynomial coeffficients

model.a = copy(x)

#calculate residual

residual!(model)

return abs.(model.residual)

end

minx, iterations, Jac, fnorm = find_broyden(model.a, x -> objective_residual!(x, model), max_iter, tol)

end

#-----------------------------------

# Solve by collocation

#-----------------------------------

@time solve_optgrowth!(model)

#-------------------------------

# Compare with the true solution

#-------------------------------

α = 0.4

β = 0.96

μ = 0

s = 0.1

c1 = log(1 - α * β) / (1 - β)

c2 = (μ + α * log(α * β)) / (1 - α)

c3 = 1 / (1 - β)

c4 = 1 / (1 - α * β)

# True optimal policy

c_star(y) = (1 - α * β) * y

# True value function

v_star(y) = c1 + c2 * (c3 - c4) + c4 * log.(y)

fig, ax = subplots(figsize=(9, 5))

ax[:set_ylim](-35, -24)

ax[:plot](model.grid, model.w_func.(model.grid), lw=2, alpha=0.6, label="Approximated (collocation)", linestyle = "--")

ax[:plot](model.grid, v_star.(model.grid), lw=2, alpha=0.6, label="Exact value")

ax[:legend](loc="lower right")

savefig("collocation.png")

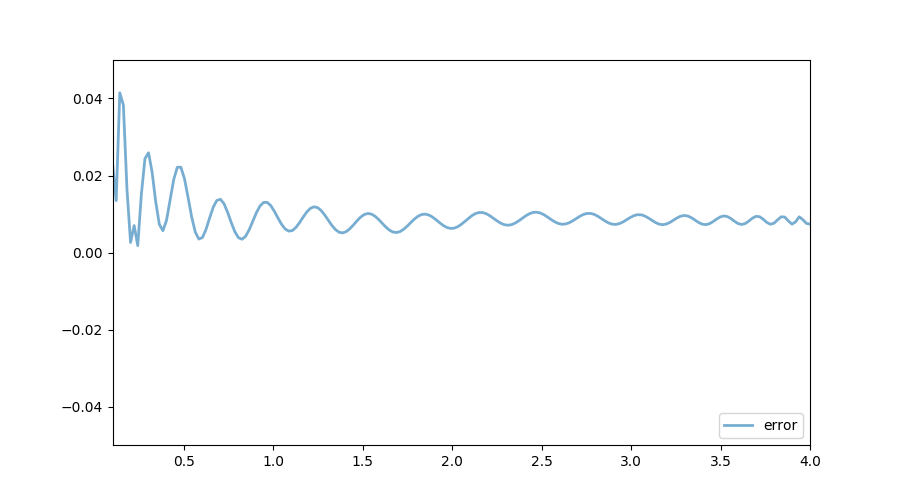

fig, ax = subplots(figsize=(9, 5))

ax[:set_xlim](0.1, 4.0)

ax[:set_ylim](-0.05, 0.05)

ax[:plot](model.grid, abs.(model.w_func.(model.grid) -v_star.(model.grid)), lw=2, alpha=0.6, label="error")

ax[:legend](loc="lower right")

savefig("error_collocation.png")

Output

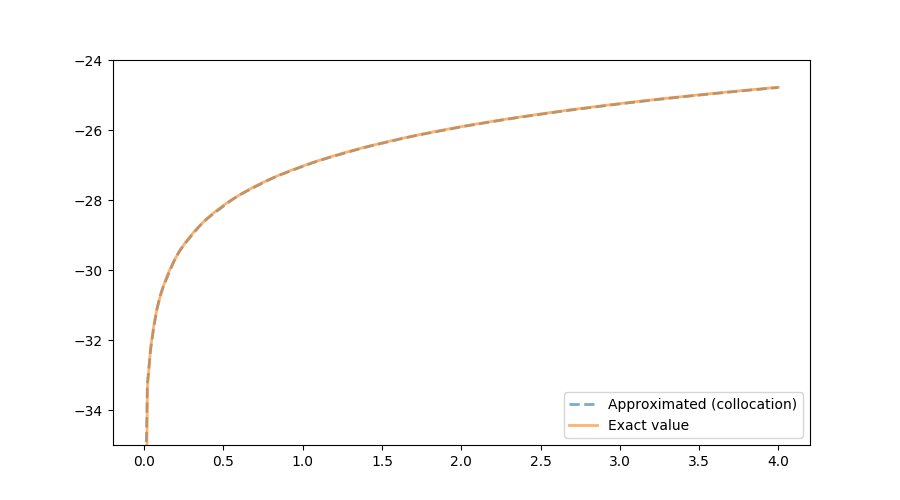

The following figure shows the exact function and the one calculated using the collocation method. In terms of accuracy, both VFI and the collocation method generate reliable results.

In terms of speed, it turns out that the value function iteration implementation is much faster. One reason seems to be the efficiency associated with the package Interpolations: it is more than 20 times faster to evaluate $w$ using the package Interpolations rather than using the package CompEcon:

#using Interpolations

#--------------------

@time for i=1:1000000

model.w_func.(model.grid[1])

end

#0.230861 seconds (2.00 M allocations: 30.518 MiB, 1.28% gc time)

#using CompEcon

#--------------

@time for i=1:1000000

model.w_func.(model.grid[1])

end

# 4.998902 seconds (51.00 M allocations: 3.546 GiB, 13.39% gc time)

Implementation using ApproxFun

Significant speed-gains can be obtained by using the package ApproxFun, as illustrated by the code below. Computing time is divided by approximately $5$ compared to the implementation using CompEcon. Yet, the value function iteration implementation is still the fastest one. One bottleneck seems to be the calculation of the Jacobian by finite differences when using Broyden’s method. It is likely that using automatic differentiation would further improve results.

#---------------------------------------------

# Julien Pascal

# Solve the stochastic optimal growth problem

# using the collocation method

# Implementation using ApproxFun

#---------------------------------------------

using QuantEcon

using Optim

using CompEcon

using PyPlot

using Interpolations

using FileIO

using ApproxFun

using ProfileView

type optGrowthCollocation

w::Array{Float64,1}

β::AbstractFloat

grid::Array{Float64,1}

u::Function

f::Function

shocks::Array{Float64,1}

Tw::Array{Float64,1}

σ::Array{Float64,1}

el_k::Array{Float64,1}

wl_k::Array{Float64,1}

compute_policy::Bool

order_approximation::Int64 #number of element in the functional basis along each dimension

functional_basis_type::String #type of functional basis

fspace::Dict{Symbol,Any} #functional basis

fnodes::Array{Float64,1} #collocation nodes

residual::Array{Float64,1} #vector of residual. Should be close to zero

a::Array{Float64,1} #polynomial coefficients

fApprox::ApproxFun.Fun{ApproxFun.Chebyshev{ApproxFun.Segment{Float64},Float64},Float64,Array{Float64,1}}

w_func::Function

tol::Float64

end

#####################################

# Function that find a solution

# to f(x) = 0

# using Broyden's "good" method

# and simple backstepping procedure as described

# in Miranda and Fackler (2009)

#

# input :

# --------

# * x0: initial guess for the root

# * f: function in f(x) = 0

# * maxit: maximum number of iterations

# * tol: tolerance level for the zero

# * fjavinc: initial inverse of the jacobian. If not provided, then inverse of the

# Jacobian is calculated by finite differences

# * maxsteps: maximum number of backsteps

# * recaculateJacobian: number of iterations in-between two calculations of the Jacobian

#

# output :

# --------

# * x: one zero of f

# * it: number of iterations necessary to reached the solution

# * fjacinv: pseudo jacobian at the last iteration

# * fnorm: norm f(x) at the last iteration

#

#######################################

function find_broyden(x0::Vector, f::Function, maxit::Int64, tol::Float64, fjacinv = eye(length(x0));

maxsteps = 5, recaculateJacobian = 1)

println("a0 = $(x0)")

fnorm = tol*2

it2 = 0 #to re-initialize the jacobian

################################

#initialize guess for the matrix

################################

# with Calculus

#--------------

fjacinv_function = x-> Calculus.finite_difference_jacobian(f, x)

# If the user do not provide an initial guess for the jacobian

# One is calculated using finite differences.

if fjacinv == eye(length(x0))

################################################

# finite differences to approximate the Jacobian

# at the initial value

# this is slow. Seems to improve performances

# when x0 is of high dimension.

println("Calculating the Jacobian by finite differences")

#@time fjacinv = Calculus.finite_difference_jacobian(f, x0)

@time fjacinv = fjacinv_function(x0)

println("Inverting the Jacobian")

try

fjacinv = inv(fjacinv)

catch

try

println("Jacobian non-invertible\n calculating pseudo-inverse")

fjacinv = pinv(A)

catch

println("Failing Calculating the pseudo-inverse. Initializing with In")

fjacinv = eye(length(x0))

end

end

println("Done")

else

println("Using User's input as a guess for the Jacobian.")

end

fval = f(x0)

for it=1:maxit

it2 +=1

#every 30 iterations, reinitilize the jacobian

if mod(it2, recaculateJacobian) == 0

println("Re-calculating the Jacobian")

fjacinv = fjacinv_function(x0)

try

fjacinv = inv(fjacinv)

catch

try

println("Jacobian non-invertible\n calculating pseudo-inverse")

fjacinv = pinv(A)

catch

println("Failing Calculating the pseudo-inverse. Initializing with In")

fjacinv = eye(length(x0))

end

end

end

println("it = $(it)")

fnorm = norm(fval)

if fnorm < tol

println("fnorm = $(fnorm)")

return x0, it, fjacinv, fnorm

end

d = -(fjacinv*fval)

fnormold = Inf

########################

# Backstepping procedure

########################

for backstep = 1:maxsteps

if backstep > 1

println("backstep = $(backstep-1)")

end

fvalnew = f(x0 + d)

fnormnew = norm(fvalnew)

if fnormnew < fnorm

break

end

if fnormold < fnormnew

d=2*d

break

end

fnormold = fnormnew

d = d/2

end

####################

####################

x0 = x0 + d

fold = fval

fval = f(x0)

u = fjacinv*(fval - fold)

#Update the pseudo Jacobian:

fjacinv = fjacinv + ((d-u)*(transpose(d)*fjacinv))/(dot(d,u))

println("a$(it) = $(x0)")

println("fnorm = $(fnorm)")

if isnan.(x0) == trues(length(x0))

println("Error. a$(it) = NaN for each component")

x0 = zeros(length(x0))

return x0, it, fjacinv, fnorm

end

end

println("In function find_broyden\n")

println("Maximum number of iterations reached.\n")

println("No convergence.")

println("Returning fnorm = NaN as a solution")

fnorm = NaN

return x0, maxit, fjacinv, fnorm

end

function optGrowthCollocation(;w = Array{Float64,1}[],

α = 0.4,

β = 0.96,

μ = 0,

s = 0.1,

grid_max = 4, # Largest grid point

grid_size = 200, # Number of grid points

shock_size = 250, # Number of shock draws in Monte Carlo integral

Tw = Array{Float64,1}[],

σ = Array{Float64,1}[],

el_k = Array{Float64,1}[],

wl_k = Array{Float64,1}[],

compute_policy = true,

order_approximation = 40,

functional_basis_type = "chebychev",

)

grid_y = collect(linspace(1e-4, grid_max, grid_size))

shocks = exp.(μ + s * randn(shock_size))

# Utility

u(c) = log.(c)

# Production

f(k) = k^α

el_k, wl_k = qnwlogn(10, μ, s^2) #10 weights and nodes for LOG(e_t) distributed N(μ,s^2)

lower_bound_support = minimum(grid_y)

upper_bound_support = maximum(grid_y)

n_functional_basis = [order_approximation]

if functional_basis_type == "chebychev"

fspace = fundefn(:cheb, n_functional_basis, lower_bound_support, upper_bound_support)

else

error("functional_basis_type has to be \"chebychev\" ")

end

fnodes = funnode(fspace)[1]

residual = zeros(size(fnodes)[1])

a = ones(size(fnodes)[1])

tol = 0.001

fApprox = (Fun(Chebyshev((minimum(grid_y))..(maximum(grid_y))), a))

#fApprox = (Fun(Chebyshev(0..maximum(model.grid)), a))

w_func = x-> fApprox(x)

w = ones(size(fnodes)[1])

Tw = ones(size(fnodes)[1])

σ = ones(size(fnodes)[1])

optGrowthCollocation(

w,

β,

grid_y,

u,

f,

shocks,

Tw,

σ,

el_k,

wl_k,

compute_policy,

order_approximation,

functional_basis_type,

fspace,

fnodes,

residual,

a,

fApprox,

w_func,

tol

)

end

function residual!(model::optGrowthCollocation)

model.fApprox = (Fun(Chebyshev((minimum(model.grid))..(maximum(model.grid))), model.a))

model.w_func = x-> model.fApprox(x)

function objective(c, y)

expectation = 0.0

for k = 1:length(model.wl_k)

expectation += model.wl_k[k]*(model.w_func(model.f(y - c) * model.el_k[k]))

end

- model.u(c) - model.β * expectation

end

# Loop over nodes

for i in 1:size(model.fnodes)[1]

y = model.fnodes[i,1]

res = optimize(c -> objective(c, y), 1e-10, y)

if model.compute_policy

model.σ[i] = Optim.minimizer(res)

end

model.Tw[i] = - Optim.minimum(res)

model.w[i] = model.w_func(y)

model.residual[i] = - model.w[i] + model.Tw[i]

end

end

function solve_optgrowth!(model::optGrowthCollocation;

tol=1e-6,

max_iter=500)

# Initialize guess for coefficients

# by giving the "right shape"

# ---------------------------------

function objective_initialize!(x, model)

#update polynomial coeffficients

model.a = copy(x)

model.fApprox = (Fun(Chebyshev((minimum(model.grid))..(maximum(model.grid))), model.a))

model.w_func = x-> model.fApprox(x)

return abs.(model.w_func.(model.fnodes[:,1]) - 5.0 * log.(model.fnodes[:,1]))

end

minx, iterations, Jac0, fnorm = find_broyden(model.a, x -> objective_initialize!(x, model), max_iter, tol)

# Solving the model by collocation

# using the initial guess calculated above

#-----------------------------------------

function objective_residual!(x, model)

#update polynomial coeffficients

model.a = copy(x)

#calculate residual

residual!(model)

return abs.(model.residual)

end

minx, iterations, Jac, fnorm = find_broyden(model.a, x -> objective_residual!(x, model), max_iter, tol, recaculateJacobian = 1)

end

#-----------------------------------

# Solve by collocation

#-----------------------------------

model = optGrowthCollocation(functional_basis_type = "chebychev")

@time solve_optgrowth!(model)

# 15.865923 seconds (329.12 M allocations: 4.977 GiB, 5.55% gc time)

#-------------------------------

# Compare with the true solution

#-------------------------------

α = 0.4

β = 0.96

μ = 0

s = 0.1

c1 = log(1 - α * β) / (1 - β)

c2 = (μ + α * log(α * β)) / (1 - α)

c3 = 1 / (1 - β)

c4 = 1 / (1 - α * β)

# True optimal policy

c_star(y) = (1 - α * β) * y

# True value function

v_star(y) = c1 + c2 * (c3 - c4) + c4 * log.(y)

fig, ax = subplots(figsize=(9, 5))

ax[:set_ylim](-35, -24)

ax[:plot](model.grid, model.w_func.(model.grid), lw=2, alpha=0.6, label="approximate value function")

ax[:plot](model.grid, v_star.(model.grid), lw=2, alpha=0.6, label="true value function")

fig, ax = subplots(figsize=(9, 5))

ax[:set_xlim](0.1, 4.0)

ax[:set_ylim](- 0.05, 0.05)

ax[:plot](model.grid, abs.(model.w_func.(model.grid) -v_star.(model.grid)), lw=2, alpha=0.6, label="error")

ax[:legend](loc="lower right")